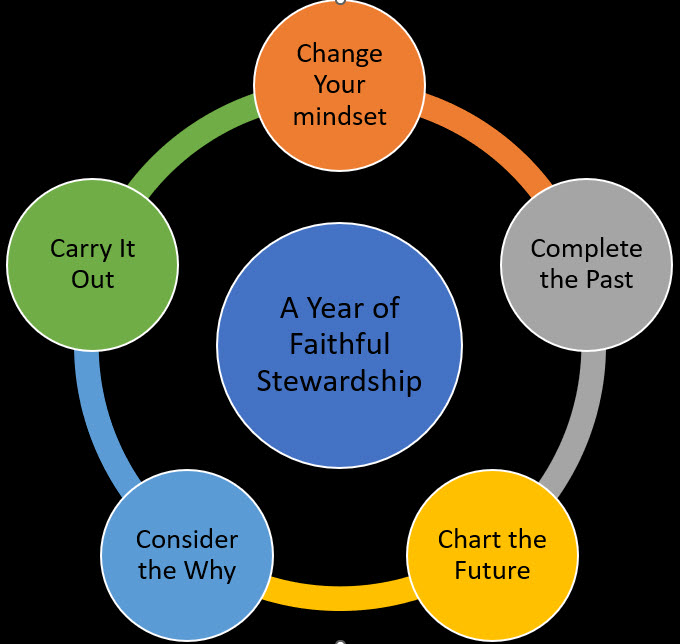

Contents

- Change Your Mindset

- Complete the Past

- Where did you want to be?

- How far did you get?

- Why are you where you are?

- What adjustments do you need to make?

- Chart the Future

- Determine your Priorities

- Define SMARTER goals

- Devise a Plan

- Consider Your Why

- The Macro Why: Love for God

- The Micro Whys: Personal Priorities

- Carry It Out

- Keep a Spending Record

- Review Spending Regularly

- Make Adjustments

- Faithful Stewardship Can Start Any Time!

Every so often, we’re made aware that we’re not where we wanted to be. This is especially true as one year ends and another begins. If we’re honest, we look over the past year with a tinge of regret. We didn’t improve our health like we wanted to. We didn’t make much of a dent in our debt. We can’t identify any significant spiritual or intellectual growth. It can feel like we failed.

At the same time, we look forward to the new year. It’s a year full of promise and possibilities. But then, so was the year we just completed. How can we make the coming year different?

In this article, we’ll outline a process for creating a year that looks different than last year in the area of stewardship. We’ll apply Michael Hyatt’s “Best Year Ever” process to our finances and put in place a plan to pursue financial freedom and grow in faithfulness to God in our stewardship.

Let’s begin with a couple key truths. First, God’s grace covers all our shortcomings – including our financial ones. Maybe we spent too much on non-essentials and didn’t make significant progress on reducing debt. Maybe we didn’t give as generously as we had hoped to. Maybe we weren’t disciplined in saving. God forgives all of this.

Second, part of God’s grace is that he doesn’t leave us in the midst of our failures. He wants to teach us, to grow us in Biblical wisdom, and to empower us toward more faithful stewardship. This is going to require some work on our part, but it’s work empowered by the Holy Spirit. So let’s dig in.

Change Your Mindset

Many of us find ourselves discouraged by what Michael Hyatt refers to as limiting beliefs. In the area of finances, some of these might be:

- “I don’t make enough money to make ends meet and also give generously.”

- “I’ll never get out of debt.”

- “I have too many bills; I can’t set any money aside for savings,”

- “I can’t live on a budget.”

Beliefs like this lead us into discouragement, doubt, and despair. And they’re usually based on past experience. We didn’t make progress on debt or savings; we set a budget but couldn’t live on it. We didn’t have enough left over to give as generously as we wanted.

But here’s the thing: Our past doesn’t determine our future. We may indeed have failed in all of these areas and more in the past, but that doesn’t mean that continued failure is inevitable. By the strength of the Holy Spirit, we have agency to change course and pursue a different future.

This begins by replacing our limiting beliefs with liberating truths. Some examples might be:

- “I have enough resources to meet all my needs and also to give back to God.”

- “With discipline and planning, by God’s grace, I can get out of debt.”

- “God has provided enough for me to pay my bills and also to save wisely.”

- “I can create and live by a workable budget.”

Of course, some of these statements reflect more faith than experience. The writer to the Hebrews reminds us: “Now faith is being sure of what we hope for and certain of what we do not see” (Hebrews 11:1). We need God to give us faith to believe that things can change.

A Mindset of Abundance

It’s easy to get discouraged over the things we lack, or over difficulties we face. Marketers strive to create discontentment and program us to think in terms of scarcity. They encourage us to look at what others have and to want what we don’t have. Our culture constantly bombards us with messages that promote greed and materialism. Paul called this idolatry (Ephesians 5:5; Colossians 3:5).

But faith leads to a different response. Faith teaches us to rely on God for our provision (Psalm 145:15-16). It promotes contentment over greed, patience over instant gratification, and trust over worry. And while faith is a gift from God, we have a role to play in growing and living by that faith.

Pray with Thanksgiving

Do not be anxious about anything, but in everything, by prayer and petition, with thanksgiving, present your requests to God. And the peace of God, which transcends all understanding, will guard your hearts and your minds in Christ Jesus.

Philippians 4:6-7

We begin to cultivate a mindset of abundance through prayer – specifically, prayer with thanksgiving. Have you ever prayed about something but not felt God’s peace afterward? If we’re honest, most of us have – repeatedly. Prayer can become a sort of “sanctified worry” if it’s not accompanied by thanksgiving.

We give thanks in two ways: first, we thank God for the answers he’s already given. The Psalmist often recounts God’s past provision in the context of praying for ongoing protection, deliverance, etc. As we remember the ways God has answered prayer in the past, our faith is strengthened to believe he will continue to take care of us.

Second, we thank God for the answers he has yet to give. When Jesus prayed to God for Lazarus’ resurrection, he began the prayer with thanksgiving that God heard him – and this was before Lazarus was raised (John 11:41-42).

Praying with thanksgiving also helps us to keep our motivations pure. James tells us that prayer isn’t answered if it’s from the wrong motives (James 4:1-3). An attitude of thanksgiving for what God has done and what he will yet do tends to guard our hearts against selfish motivations because it keeps our focus on God rather than on our specific requests.

Rely on God’s Provision

Therefore I tell you, do not worry about your life, what you will eat or drink; or about your body, what you will wear. Is not life more important than food, and the body more important than clothes?

Matthew 6:25

Jesus taught us to pray for God to meet our needs. Twice in the Sermon on the Mount he tells us to ask God to provide for our needs (Matthew 6:11; Matthew 7:7-8). And between these two exhortations, Jesus teaches us not to worry because God will provide. God takes care of the lilies of the field and the birds of the air. This doesn’t mean that we don’t work to meet our needs, but in the context of that work, we recognize God as the ultimate source of our provision.

Relying on God’s provision frees us up to seek God’s kingdom first (Matthew 6:33). In the context of stewardship, trusting in God to provide helps us to balance our giving, saving, and spending in ways that honor God and that reflect our understanding that he is the source of all we have.

Part of relying on God’s provision is realizing by faith that he has in fact provided for all our needs. That doesn’t mean that he’s always provided all that we want or taken care of us in exactly the way we pictured. But it does mean trusting that what he has provided is what is best for us.

Cultivate contentment

But he said to me, “My grace is sufficient for you, for my power is made perfect in weakness. ”

2 Corinthians 12:9

God doesn’t answer all prayers in exactly the way we ask or envision. Paul prayed multiple times for God to remove his thorn in the flesh, but God ultimately refused, insisting instead that Paul rely on God’s grace to be his strength. Our faith tends to grow most in times of adversity. Note all the adversity encountered by the heroes of faith documented in Hebrews 11!

Paul learned the secret of being content in any and every situation (Philippians 4:11-13) – including the circumstance of prayer not being answered in the way he envisioned. In 2 Corinthians 11:23-29, Paul recounts many of the trials he endured for the Gospel – trials that would make our financial difficulties seem insignificant by comparison. And yet, he was able to endure all of that with contentment. He was content when he had much and when he had little. He was content when churches were planted and thriving and content when he was suffering persecution.

This attitude of contentment is a great antidote to materialism. And materialism is perhaps the single biggest obstacle to financial freedom and Biblical stewardship. If we can learn to adopt a posture of contentment in all we do, we have a much better chance of changing direction financially.

Complete the Past

A popular definition of insanity is doing the same thing over and over and expecting different results. In order for the coming year to be different, we typically need to break with some patterns of the past. But how do we identify what needs to change? Start with some key questions.

Where did you want to be?

What goals did you set last year? Or, if you didn’t set specific goals, where did you envision being financially at the end of the year? Did you expect to accomplish certain milestones (eg, save $10,000 or retire $8,000 of debt)? Did you expect to have certain rhythms established (eg, monthly giving of a certain amount or regular financial discussions with your spouse)?

Be honest with yourself. Maybe you didn’t actually sit down and write out a budget last year, but you probably had some idea in mind of where you hoped to be financially. Write down what comes to mind, whether they were intentional goals from the previous year or just a picture of where you hoped you would be.

How far did you get?

Did you meet your goals? Candidly evaluate where you are against where you hoped to be. Where did you succeed? Where did you fall short? Were there some areas where you made good progress and others where you struggled? Did you actually move in the wrong direction in some areas? Understanding clearly where you made progress and how much progress you made is a key step to creating a year of faithful stewardship.

Why are you where you are?

Identify the contributing factors to your successes and failures. Ask some key questions about the previous year (or whatever period), like:

- Did you fully understand your goals?

- Were these the right goals in the first place?

- Did you regularly check in with your goals to monitor progress?

- What did you accomplish that you’re most proud of?

- What disappointments or regrets do you have?

- What was missing?

- What mistakes did you make?

- What obstacles did you encounter? How prepared were you?

- What surprised you?

What adjustments do you need to make?

Start with prayer! Consider:

To the extent that you didn’t meet your goals,

- Is there anything you need to confess before God?

- Where do you need to ask for wisdom?

- Are there areas in which you need God to work in your heart?

And in those areas where you succeeded,

- What do you need to thank God for?

- How should you respond to God’s provision?

As you pray through these responses, think about the questions we asked above. Consider:

- Do you need to set more or fewer goals? Do they need to be more or less aggressive?

- What obstacles should you anticipate this year?

- What patterns or rhythms do you need to consider?

- How flexible are you regarding potential sacrifices you may need to make?

Chart the future

Once you’ve adopted a steward’s mindset of gratitude and contentment, acknowledged any gaps between where you wanted to be and where you are, and identified some adjustments to make, it’s time to begin your planning. To do this, you’ll start with your financial priorities, then define some key goals, and finally create a plan to meet those goals. By the time you’re done, you’ll be ready to embark on a year of faithful stewardship.

Determine your priorities

Your financial goals should reflect your life’s priorities. These priorities have financial implications, but they’re bigger than that – they reflect key life decisions. They’ll change over time as your life changes, but it’s important to keep them in view as you think through your financial goals.

Key areas to consider include your spiritual life (including generosity from a financial standpoint), your family, location, work, life experiences, etc. For example, is it more important to have one spouse stay home or to send the children to private school (which will likely require two incomes)? How important is it to live in a good school district (which will probably increase the cost of housing)? Would you prioritize major family vacations or smaller, more frequent (but less expensive) family experiences?

For some additional thoughts on priorities, see our related article, Spending Priorities & Non-Negotiables.

Define SMARTER Goals

Identifying and writing down your goals is a key step toward achieving them. Research shows that the act of writing a goal down increases the probability of achieving that goal. Writing down our goals forces us to visualize them specifically.

You may have heard of the SMART paradigm for goal-setting. Michael Hyatt recommends a variation on this paradigm, preferring goals that are SMARTER. So as you begin to consider your financial goals for the year, keep in mind the following characteristics.

Specific

Avoid vague goals like “I want to be in better financial shape” or “I want to have more financial freedom”. These goals don’t push us in a direction. On the other hand, a goal like “I want to reduce debt” is specific enough to suggest actions (using cash instead of continuing to use credit cards, paying more than minimum payments, etc.).

Measurable

A goal such as “reduce debt” is specific, but not measurable because it doesn’t have a target. Reduce by how much? Is a $10 reduction in debt over the period of a year success? We’d probably agree that it’s not. So consider setting a measurable goal, such as “I want to reduce debt by $10,000 this year” or maybe “I want to pay off credit cards X, Y, and Z this year while taking on no new debt”.

Actionable

Write your goals in such a way as to indicate actions to be taken, using active verbs rather than passive verbs. A goal like “Be more disciplined in spending” doesn’t suggest any specific action. But a goal like “Establish a monthly budget” gives a specific action step to take.

Risky

This is where Hyatt differs from the typical SMART goals, where the “R” stands for Realistic. Our goals should be difficult enough that they are worth celebration when we meet them. They should be goals that push us, not goals that we would accomplish just through normal living. Risky goals require faith. They should drive us to our knees in prayer, dependent on God for his strength and provision. At the same time, they shouldn’t be delusional. They should be difficult, not impossible, to attain.

Research shows that setting difficult goals tends to lead to greater achievement than setting goals that are easily attainable. The goal may not be achieved as written, but even getting partially there often exceeds the accomplishment of meeting a less challenging goal.

For example, a goal of “Establish an Emergency Savings fund of $2000 by the end of the year” isn’t all that risky for someone making $100,000 a year. The nature of Emergency Savings should drive us to a riskier goal, maybe something like “Establish an Emergency Savings fund of $1000 within a month and fund it to $2,000 within 3 months.”

Time-bound

Goals need a target date. “Reduce debt by $10,000” needs a deadline date in order to encourage action. If the date is far enough out, we tend to procrastinate. But we take action when there’s a challenging date.

One of the keys to setting deadlines for goals is not to stack deadlines too close. For example, it might not be wise to set a goal for building an emergency fund and another goal for retiring all debt for the same date. In some cases, it will be necessary to prioritize goals, setting the deadlines far enough apart so that they can all be met.

Not all goals are “achievement” goals that have a specific deadline. Some goals can better be thought of as “habit” goals – objectives that describe patterns rather than specific achievements. An example would be, “I will write down my expenses for the day every night when I get home.” This defines the frequency and the time when the action will be taken. The more specific the definition of the habit, the better chance we have of meeting the goal.

Exciting

Goals should motivate us and keep our attention. They should be worth celebrating when we accomplish them – which is one of the reasons they need to be a bit risky.

Note that part of the excitement can be generated by setting milestone goals, helping us to stay motivated on the way to the larger goals. The “debt snowball” is a good example of this, where we set goals for retirement of individual credit cards and loans on the way to being completely out of debt.

Relevant

Relevant goals are meaningful in our current financial situation. For example, it may not make sense to set a goal for investing while we’re still in debt. In later life, a goal for increasing saving might not be relevant if we’ve saved enough for retirement.

Relevant goals can be set in the areas of saving, giving, spending, earning, and debt retirement. For example, you might have a goal of saving a certain amount by the end of the year. Or maybe a goal of working up to contributing a certain amount of your paycheck toward a retirement account with an employer match by the end of the year. Or maybe a goal of giving a certain percentage of your income over the course of the year. The goals you set should be meaningful and relevant for you.

Devise a Plan

With your priorities in mind and your goals established, create a plan to get you there. This plan should incorporate earning, spending, giving, saving, and debt retirement as needed.

The plan you create should be realistic given your goals and priorities. If you have spending records for a month or two, use these along with your goals to inform your spending plan. For example, if you’ve been averaging $1,000 a month spending on food, you might set a goal of spending $800 a month, but a goal of $500 a month is probably not realistic or even risky – it’s simply beyond reach. If you don’t have good records, you’ll need base your plan on estimates of spending. Monthly bills and statements will help. Here’s a general rule of thumb: If you don’t know how much you’re spending in a particular area, it’s probably more than you think it is!

Creating a Spending Plan takes work, but it’s the best way to flesh out your priorities and financial goals. A Spending Plan turns hopes and wishes into actual goals you can work toward. Remember, “If you aim at nothing, you’re sure to hit it!”

If you’d like some help getting started, see our related article, How to Create a Spending Plan.

Consider your why

Determining our priorities, setting goals, and creating a plan can be exciting. It’s like the beginning of a road trip full of the promise of adventure. But achieving a year of faithful stewardship isn’t easy. Most likely, if you’ve thought through the steps we’re outlining, you’ve already foreseen some obstacles and difficulties. And nearly every year brings with it at least one surprise – an appliance breaking down, an unexpected car or home repair, a significant illness or injury. When these things occur, it can be easy to get discouraged.

At this point, we need to remember the why – the reasons we’re doing what we’re doing. Without a strong handle on the why, we’ll tend to give up on our goals and on the priority of Biblical stewardship. We’ll get bogged down in what Michael Hyatt calls the “messy middle” – that part after the excitement wears off when we’re slogging through obstacles and difficulties.

Let’s consider the why on a couple of different levels: The macro why and the micro whys.

The Macro Why: Love for God

“Do not store up for yourselves treasures on earth, where moths and vermin destroy, and where thieves break in and steal. But store up for yourselves treasures in heaven, where moths and vermin do not destroy, and where thieves do not break in and steal. For where your treasure is, there your heart will be also. … “No one can serve two masters. Either you will hate the one and love the other, or you will be devoted to the one and despise the other. You cannot serve both God and money.”

Matthew 6:19-21, 24

Our relationship to money has a large impact on our relationship with God. Jesus makes a surprising statement in the passage above. We’d expect that we would put our treasure where our hearts already are – but Jesus tells us that it actually works the opposite way: Our hearts follow our treasure.

Further, Jesus tells us that we must choose whether we will serve God or money. What are some of the ways we serve money?

- By hoarding – saving more than we need because we’ve placed our security in money rather than God (Luke 12:16-21; 1 Timothy 6:17)

- Through greed and materialism – accumulating possessions instead of sharing with others (Ephesians 5:5; Colossians 3:5)

- By consumerism – consuming all we have carelessly (Proverbs 21:20)

When we’re not intentionally managing our money as stewards, chances are we’re drifting in one of the three above directions.

Most of us would admit that we long to walk more closely with God, to grow in our love for God and for others. Jesus gives us a key to moving in that direction – serving God with our finances. And that means we need to be intentional about how we use the money God puts in our possession.

The Micro Whys – Personal Priorities

Suppose you set a goal of retiring half your credit card debt this year. You know that in order to do that, you’ll need to avoid further use of credit cards. But then, the sofa that you’ve been wanting for some time goes on sale and you’re tempted to take on more debt in order to buy it.

There are lots of reasons to buy the sofa – maybe your current one is worn out and the new one fits your living room better. And if you don’t know the reasons why you want to retire debt, you’ll likely end up with a new sofa – along with several hundred dollars (or more) of additional debt. So it’s important to know why you want to retire debt.

Of course, there are Scriptural foundations like being free from enslavement to creditors (Proverbs 22:7). But on top of that, what are your motivations? Maybe they include stopping phone calls from creditors or maybe they’re based on what you could do with additional money if you weren’t making credit card payments. Maybe you want to purchase a house but you have too much current debt to get a loan. Identifying your motivations will help you stay on track despite all the distractions that might come up.

Carry It Out

You’ve planned a year of faithful stewardship. You’ve identified your priorities and your motivations for those priorities. But now, how do you make it happen? Here are a few key steps.

Keep a Spending Record

A Spending Plan is like a map. It shows you where you want to go. But a map doesn’t help if you don’t know where you are.

A Spending Record is more like a GPS. It tells you where you are so that you can make any adjustments you need to. So, suppose you’ve planned to spend $600 a month on groceries, for example. That might be a good plan, but are you following it? The Spending Record enables you to answer that question.

Create and maintain a spending record that matches up to your spending plan. Use the same categories, and as far as possible, try to get to the same level of detail as your spending plan. Remember, the goal is to understand whether or not you’re on track with your plan.

If you need help getting started with a spending record, please see our related article, How to Track & Categorize Spending.

Review Spending Regularly

The biggest value of the spending record is in reviewing it against your plan. It’s important to know that you’re spending $800 a month on groceries – but the real significance of the data point is in comparing it to what you planned to do. Did your plan allot $800 a month for groceries? Then you’re doing great! Did you allot $600 a month? Then you need to make some adjustments.

Evaluating your spending against your plan will help identify places where you’re overspending (and there will be some!) and maybe other places where you’re ahead of plan. One thing to keep in mind: Some categories won’t have spending every month. So, for example, if you’ve allocated $50 a month for auto maintenance, you might go a month or more without spending in that category.

Make Adjustments

Once you’ve identified areas where you’re over- or under-spending, it’s time to determine what adjustments are needed and then to make those adjustments. This is where you reap the real benefits of the spending plan and spending record. In each category where your spending was significantly different than plan, determine which of the following is true:

No adjustment needed

In some cases, you won’t need to make adjustments. Maybe you had a bad month in a particular category after a string of good months. Maybe you’re evaluating a category where you don’t spend every month (like clothes, auto maintenance, or gifts) – in that case, you’ll have some months where you spend more than the plan and others in which you don’t spend at all. Pay attention to the trend over time and evaluate over a period of multiple months.

Adjust your spending

If you’re consistently over-spending a particular category, you may need to adjust your spending habits. Are you eating out more than you can afford? Buying more clothes than you need? If you’re overspending in one or more areas, one of two things is likely happening: you’re taking on additional debt, or you’re failing to set aside money you should be saving for spending in other categories or for longer-term goals.

Adjust your plan

In some cases, you’ll find that it’s the spending plan that needs adjusting. Perhaps your original plan wasn’t realistic and you need to adjust it to reflect your actual spending more closely. Or maybe your priorities or life circumstances have changed and the plan needs to be updated to reflect those changes.

Whatever the case, remember that your spending plan isn’t set in stone; it’s there to serve you, not the other way around. When you make adjustments to the plan, be sure that your updated plan reflects your priorities.

Faithful Stewardship can start any time!

While many of us evaluate where we’ve been and where we’re going at the turn of the year, stewardship transformation can begin at any point. Here are a final few tips to help you get started.

Start now

When Jesus called his disciples to follow him, he never said, “start following me when you’re ready.” He called for immediate responses every time.

When it comes to transforming your finances, don’t wait! You might not be quite ready to put a spending plan together yet. But you can start by understanding where you are and why, beginning a spending record, and praying through your financial priorities.

If the task seems daunting, consider breaking it down into months to get started. Here’s a recommended first quarter of activity:

- Month 1: Establish an accurate, complete spending record. You need at least a month’s worth of expenses to create an effective spending plan. Pray through your priorities and your financial goals (with your spouse, if you’re married!). Start setting aside an Emergency Savings fund if you don’t have one. Check out some of our related articles below for additional ideas.

- Month 2: Create a spending plan based on your actual spending, your life priorities, and your financial goals. Complete funding your Emergency Savings to 2% of your annual gross income. Continue your spending record.

- Month 3: Continue the spending record and compare your actual spending to your plan. Make adjustments as needed. Create an updated spending plan by the end of the month based on the adjustments you made. With an Emergency Savings fund fully funded, focus on maximizing any employer match toward a retirement account and reducing consumer debt.

Anticipate difficulties

The coming year won’t be perfect. Unexpected expenses will occur. Or you’ll find that your original plan wasn’t quite realistic, or that it isn’t helping you attain your financial and life goals. Don’t let this stop you from creating a plan or from making the ongoing adjustments. As we said earlier, if you aim at nothing, you’re sure to hit it.

A year of faithful stewardship doesn’t have to look like 12 months of hitting every spending goal you set. Aim for progress over perfection and keep going!

Handle with prayer

We end where we started. The journey to financial freedom and Biblical stewardship is one that requires God’s grace and our willingness to grow. And both of these call for prayer! Prayers of confession when we’ve made a bad decision or failed to be as disciplined as we should; prayers of thanksgiving for God’s provision; prayers for guidance in determining priorities and creating a spending plan; prayers for strength and discipline to follow the plan.

A year of faithful stewardship is not a one-time goal; it’s a springboard to a lifetime of managing our finances in ways that honor God. Whether it’s the beginning of the year or not, start today on this key discipleship journey!

Want help to apply the key steps in this article and grow in your stewardship? Check out the FreedUp app!