Your congregation is learning about money. They’re learning from marketers, with their constant barrage of enticements to purchase the products that they profit from. They’re learning from financial advisers, with their bent toward saving and investing. The problem is, neither of these sources originate in a Biblical worldview.

Whether the overall message is “spend now and enjoy life” or “save now so you can spend later”, the ultimate focus of the message is the individual. On the one hand, we’re bombarded with inducements to spend and enjoy ourselves (regardless of whether we can afford it). Look at the commercials – everyone who purchases anything is happy and content. No buyer’s remorse there!

On the other hand, we’re cautioned that we need to focus on saving and investing (usually by those who make profits from the investment transactions). These messages typically portray motivations of fear (you may not have enough later if you don’t start investing now) or delayed gratification (save now so that you can live it up when you retire).

But none of these messages encourage us to consider how God would have us manage the resources He has entrusted to us. The worldview behind these messages is a self-centered one, not a God-centered one. The only place where our congregations will get a God-centered view of money is the Church. And that’s why training our congregations in Biblical stewardship is so important.

Scripture teaches us that in Christ, we have a new life (Galatians 2:20) and commands us, as a result, to put the old earthly ways of thinking and acting behind us (Romans 12: 1-2; Colossians 3:1-2; Ephesians 4:20-24). And managing our finances is a critical area in which we need to do this. As with most other areas of life, the Christian’s view and use of money should look different than the world’s.

In the Sermon on the Mount, Jesus warned that we have to choose whom we would serve. On the one hand was God. Jesus could have put anything he wanted to on the other side of the scale. What did he choose? Money! (Matthew 6:24). Money may not be the biggest obstacle that comes to our minds when we think about serving God, but Jesus recognized how critical our relationship to money is. He even listed the deceitfulness of wealth as one of the primary obstacles to the Word being fruitful in our lives (Mark 4:19).

If Jesus was this concerned about money as a rival god, then the church must disciple its people in this key area. A Biblical view of money won’t come from anywhere else.

Struggles in Stewardship training

We struggle in several ways when it comes to teaching about money. First, most churches don’t teach about money at all. Stewardship is not a common seminary topic, and many pastors don’t feel equipped to speak authoritatively about money. Additionally, money isn’t a comfortable topic, and many pastors are afraid of alienating their congregations by addressing it. This is especially true of seeker-oriented churches.

Second, when the church has talked about money, the talk tends to center only around giving – which is just one part of Biblical money management. In fact, many churches run “stewardship campaigns” – essentially equating Biblical stewardship with giving. As a result, congregants can become somewhat jaded when the topic of stewardship comes up, seeing it as a self-serving topic for the church.

Then there are the extremes. Historically, the church has often elevated asceticism as the Biblical norm for handling money. Since most people don’t live lives of deprivation, this creates dissonance between what’s being taught and what people are experiencing. And while it’s true that Jesus did call the rich young man to sell everything and give to the poor (Mark 10:17-22), this is the only occasion recorded in Scripture where He made such a demand. Jesus taught much about money without ever repeating this charge.

On the other hand is the prosperity gospel popular in some churches in America. Conflating the gospel with the American dream, some pastors preach (and assume) that God intends to bless his people with material wealth as a norm. God, of course, works in different ways in His children. He does indeed bless some with wealth – but at the same time allows others to suffer great persecution and poverty. This highly westernized version of the Gospel presumes on God’s grace and ignores the situations of the majority of believers around the world.

So we need to disciple our congregations in stewardship, but we need to teach a balanced, Biblical perspective. What are the keys to such a perspective?

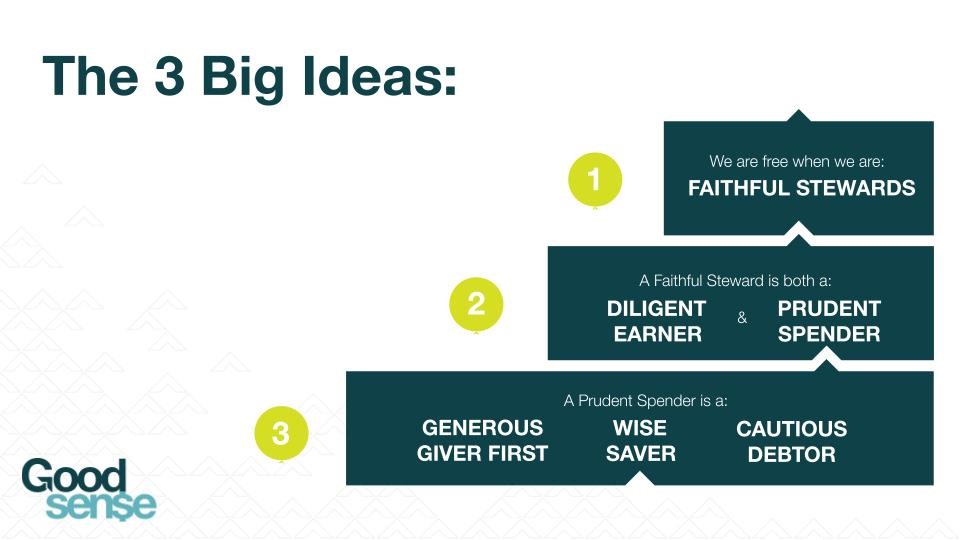

The Big Ideas

Biblical stewardship is based on three “Big Ideas”:

- We are truly free when we are faithful stewards.

- A faithful steward is both a diligent earner and a prudent spender.

- A prudent spender is a generous giver first, a wise saver, and a cautious debtor.

Let’s look a little more closely at each of these.

The Faithful Steward

A faithful steward recognizes that God is the owner of all things and that we have been entrusted with some of those things for a time to manage for his pleasure (Genesis 1:1; Exodus 19:5; Psalm 24:1; 1 Corinthians 10:26; Colossians 1:16; Hebrews 1:2-3). Faithful stewards are grateful to God because they recognize that all they have comes from him, including even the ability to earn wealth (James 1:17; 1 Timothy 6:17; Deuteronomy 8:17-18).

Faithful stewards are content, whether they have been given much or little (Philippians 4:11-13; 1 Timothy 6:6). They don’t put their hope in wealth but rather in God (1 Timothy 6:17). As a result, they serve God rather than money, storing their treasures in heaven rather than on earth (Matthew 6:20-24).

As we take seriously the responsibility to disciple our congregations in the area of finances, we will see results on multiple levels. On the individual level, members in the congregation begin to experience more freedom and peace as they learn to put money in its rightful place. They develop a sense of purpose that underlies their financial decisions. On the church level, the body tends to experience the benefits of greater generosity, as congregation members reject cultural myths about money and pursue God’s heart. And on the community level, society tends to benefit from the investment and generosity of faithful stewards.

Equipping faithful stewards

Equipping our congregations in financial discipleship starts with challenging them to understand our role as stewards rather than owners. This requires a major shift in thinking and in the focus of our hearts. The key here is to emphasize the truth that Jesus taught in Matthew 6:21 – that our hearts often follow our treasure. It’s not about waiting for God to change our hearts but rather about living in obedience to his Word and placing our treasure in heaven. By doing this, we put ourselves in a place where God can move our hearts.

As with other spiritual practices, we also need to encourage our congregations to be intentional about stewardship. This means paying attention to how we’re using the financial resources God provides. The first two servants in the parable of the talents (Matthew 25:14-30) were intentional about how they handled their master’s money. No doubt they kept track of their investments and understood which were working and which were not, and adjusted accordingly. They were diligent in their management of the master’s resources.

The Diligent Earner

God created work before the Fall to be a significant part of our lives (Genesis 1:28; 2:15). Work was made more difficult after the Fall (Genesis 3:17-19) but has always been part of God’s purpose for his people. God Himself gives us the ability to work and produce wealth (Deuteronomy 8:17-18) and calls us to be diligent earners.

Diligent earners have a Biblical view of work, understanding that work is part of the purpose for which we were created. They know that work is part of being in God’s image (John 5:17); as a result, they recognize that how they work reflects on God’s character. At the same time, they realize that their value is not in their accomplishments at work, their position, or their paycheck. Instead, they identify their value as beloved sons and daughters of God (John 3:16; Romans 5:8; 1 John 3:1).

Diligent earners work hard, but they do more than just that. They strive to make their companies and their bosses successful. They care about the end results of their work and invest not just their labor but also their expertise. Diligent earners work “with all their heart, as working for the Lord, not for men” (Colossians 3:23).

Because diligent earners are grateful, they perform their work without complaining or arguing. As a result, their attitude stands out among their peers and can even open doors for the Gospel (Philippians 2:14-16). Such a perspective is most important when the work environment is difficult. Maintaining a positive attitude when things are good is like loving those who love us – anyone can do that (Matthew 5:46). But a positive attitude in difficult times sets believers apart from the world and gives us a testimony to God’s grace.

Diligent earners get their identity from Christ rather than from their work. As a result, they don’t depend on promotions and raises to validate their worth. These tend to come over time, but diligent earners respond with gratitude rather than entitlement. Additionally, diligent earners maintain a good sense of work-life balance. They may occasionally work overtime to meet an important deadline, but they place a priority on their walk with God, time with their family and involvement in the community.

Many in our congregations have an unbalanced view of earning. They may be disinterested earners, working only out of necessity to earn a paycheck but not valuing work as something created by God for our benefit. Disinterested earners tend not to be grateful for their jobs and tend to grumble when the work environment gets difficult (which it always does!). They’re a bit like the third servant in the parable of the talents – not caring about their employers and not concerned about their own reputations at work.

On the other end of the scale are the driven earners. They may be driven by a compulsion to make money, or by a desire for advancing in their career, or by other pressures. Driven earners are all about maximizing their positions and paychecks, often at the expense of personal and family health. And nearly always at the expense of their spiritual lives.

Equipping Diligent Earners

The church benefits when its people are diligent earners, rather than disinterested or driven earners. Diligent earners care about the people they work with and work hard for their companies, which reflects well on the character of God and the reputation of the church. Diligent earners reflect a grateful attitude at work, which carries over into other areas of life. At the same time, they know how to keep work in its place, seeing it as part of a balanced life focused on God. As a result, diligent earners tend to have healthier families and the highest level of involvement in the body.

Equipping diligent earners requires that we teach a balanced, Biblical view of work as part of an overall view of stewardship. This begins with God’s creation of work as a significant part of our purpose. This purpose goes beyond a paycheck – it’s part of who we’re made to be (note that Adam and Eve never received a check for their work!). Additionally, we need to emphasize gratitude for work as a response to God’s giving us the ability to produce wealth. Finally, we need to help our congregations see work as one of the major environments in which we interact with people far from God. Our attitudes and diligence reflect God to those who are far from him.

The Prudent Spender

Earning is one side of the money equation. The other side is spending, which incorporates everything we can do with money: giving, saving, lifestyle spending, and debt retirement. Balancing all of these in a God-honoring way requires intentionality and diligence. Faithful stewards are prudent spenders.

Prudent Spenders enjoy the fruits of their labor while guarding against materialism. They recognize God as the source of all they have (James 1:17) and enjoy what he has provided with a sense of gratitude (1 Timothy 6:17). At the same time, they realize that life consists of more than possessions, so they guard against greed (Luke 12:15). They’re content with what God has provided (Philippians 4:11-13).

Prudent spenders exhibit self-control (Galatians 5:23; 1 Peter 1:13; 4:7; 2 Peter 1:6). This leads them to be intentional about their spending. They recognize that “there is a time for everything” (Ecclesiastes 3:1), including a time to spend and a time to refrain. As a result, they’re patient and able to wait for their wants to be satisfied.

Prudent spenders commit themselves to God in the way they use their resources. Whether they’re spending on lifestyle, giving, saving, or retiring debt, they see all of their finances in light of God’s provision and their own stewardship. As a result, they don’t make idols of either possessions or money.

Prudent spenders have a strong sense of priorities that guides their financial decisions. They consistently ask, “What’s the best use of this next dollar?” They have a plan and that plan guides their decisions. Supporting that plan, prudent spenders keep good financial records. They know how much they’re spending, what they’re spending it on, and how that matches up to their plan. This way, they know when the plan needs adjusting (as it inevitably will), and they make the right adjustments at the right time.

Because prudent spenders are intentional about their spending, they avoid impulse buying. They don’t tend to shop as entertainment – whether online or in stores. Instead, they shop when they’re looking for something specific that they’ve planned for. For large purchases, they weigh multiple factors as they decide on what to buy.

Finally, Prudent spenders know how much they need to live on and they live within their means. Ultimately, contentment and intentionality lead them to establish a lifestyle cap – an amount that they’ve determined that they need to live on. This lifestyle cap describes an appropriate level of spending for their situation, and frees them toward increasing generosity as their income increases.

Equipping Prudent Spenders

Churches benefit from equipping their congregation to be prudent spenders in a couple of ways. First of all, the discipline and self-control that characterize prudent spenders will show not only in their finances but also in their spiritual lives. The ability to gain control over impulses and to delay gratification reflects maturity, and this maturity often shows itself spiritually as well as financially.

Prudent spenders reject the “me-first” attitude that characterizes so much of our culture. As a result, they are typically quick to share the blessings that God has granted. In the body, this spirit of generosity develops a community of caring and sharing.

It would be easy to say that helping our congregation to become prudent spenders is a matter of getting them to cultivate hearts of contentment and gratitude and to develop a sense of purpose in their spending. But realistically, it doesn’t work this way. Scripture tells us that the heart is deceitful (Jeremiah 17:9), and as a result, being guided by our hearts often leads us in the wrong direction.

Heart change comes from God, so it begins with prayer. For the ascetic, this may be prayer for God to increase their faith in His provision or prayer to be relieved of false guilt. For the spendthrift, it may be prayer for gratitude and contentment, or prayer for healing from an emotional wound that’s triggering their spending.

In either case, Jesus said that our hearts tend to follow our treasure (Matthew 6:21), so the next step is to help people track their spending and from that to create a spending plan. Understanding where our money goes is the first step to controlling where it goes, and putting that control in place helps determine where our treasure is. Heart change will tend to follow that treasure.

The Generous Giver

It will come as no surprise that the Bible speaks more about giving than about any other area of financial stewardship. Giving both directs and reflects our hearts. On the one hand, giving directs our hearts by breaking the hold that money can have on us. On the other, it reflects our hearts by showing what we value. God calls us to be generous givers.

Generous givers give with an obedient will, a joyful attitude, and a compassionate heart. They make room for giving generously by living with gratitude and contentment, which protects them from materialism. While most believers want to be generous givers, the prudent spender’s intentionality about spending actually enables generous giving.

Many in our congregations may be grudging givers, rather than generous givers. Motivated by guilt, legalism, or a “call to action” over something they’re not passionate about, they give out of compulsion, rather than cheerfully and joyfully. This is the kind of giving that God doesn’t want. As Paul told the Corinthians, “Each of you should give what you have decided in your heart to give, not reluctantly or under compulsion, for God loves a cheerful giver” (2 Corinthians 9:7). Generosity is more a function of the giver’s heart than of the size of the gift.

Giving is the area of stewardship that most directly reflects where our hearts are and whom we’re serving (Matthew 6:21-24). Contrast the reactions of two men who encountered Jesus. Zacchaeus, on encountering the Savior, joyfully and immediately revealed the transformation of his heart by giving generously to the poor and making restitution for his past unfair tax collection practices (Luke 19:1-9). But the rich young man couldn’t part with his wealth and “went away sad” (Mark 10:17-22). The difference? Zacchaeus had made Jesus his lord, while the other man’s lord was his money.

Generous givers are grateful to God for all that they have. They understand that they are stewards of God’s possessions and rejoice in opportunities to further his kingdom. They tend to be compassionate and aware of needs around them (Acts 2:44-45; 4:32-37). They’re content with what they have, regardless of whether that is much or little (Philippians 4:12).

Generous givers make room for giving by limiting lifestyle spending. They give systematically (Proverbs 3:9) but also look for opportunities to meet specific needs (such as the collection for the church at Jerusalem). As God leads, they may give lavishly on special occasions (Matthew 26:6-13). This giving may or may not be large in amount (see Mark 12:41-44), but it represents a sacrifice on the part of the giver. The Macedonian church was characterized by this kind of giving (2 Corinthians 8:1-5).

Equipping Generous Givers

The church needs generous givers – but not primarily to meet programming budgets. Acts 2:42-47 reflects several key characteristics and habits of the early church, one of which was generosity (v. 44-45). This spirit of generosity enabled the church to fulfill two primary objectives: meeting the needs of its people (v. 45) and attracting and discipling non-believers (v47).

Generosity isn’t encouraged by focusing on building campaigns, church budgets, or even disaster relief funds. These are all important, but focusing our attention on these outcomes misses the heart of generosity. Need-based appeals are occasionally important (as Paul’s collection for the Jerusalem church), but they won’t create a heart of generosity. Instead, we must inspire gratitude and contentment in our congregations and reflect giving as a part of overall stewardship.

The Wise Saver

Giving, of course, requires first of all that the believer have something to give! That requires earning, but it also requires saving. Saving doesn’t replace faith, of course; instead, saving reflects responsible stewardship of what God has provided.

Wise savers build, preserve, and invest with discernment. They provide for the future, saving for their own needs (Proverbs 6:6-8; 21:20; 30:25) and the needs of others (1 Corinthians 16:2; see also Genesis 41). At the same time, their ultimate hope is not in their savings but in God (1 Timothy 6:17). As a result, they avoid hoarding (Luke 12:16-21).

Wise savers are intentional about how they manage their finances. Because saving is an important goal, they dial back on spending in order to make a priority out of setting aside for the future. Wise Savers understand the value of delayed gratification – a very counter-cultural characteristic! They practice patience and planning.

Wise savers anticipate the future. They recognize, for example, that items like appliances and automobiles will eventually need to be replaced and they prepare by saving up replacement funds, rather than borrowing in the moment when the need arises. They also realize that unexpected events will occur and, rather than relying on credit, they prepare for these events by saving. Finally, wise savers realize that a time is likely to come when they are no longer earning enough to meet their needs, so they prepare with long-term saving for those years.

Equipping Wise Savers

The church needs Wise Savers. We need brothers and sisters who have accumulated enough margin to help others in need, as we see in the early church (Acts 2:44-45; 4:32-37). We need believers who can model contentment, patience, and self-control in the face of a culture that pulls us in the other direction. So how do we equip our people to be Wise Savers?

As always, equipping the saints begins with God’s Word. While most churches will give the occasional sermon on giving, relatively few teach the wisdom of Scripture when it comes to saving. Culture steps into this vacuum of teaching and directs people – including believers – to spend all they have (and more!). Our culture promotes instant gratification and pushes the idea that saving is futile and unnecessary. The story of Joseph saving up grain in Egypt in preparation for a famine (Genesis 41) shows how God can work through wise saving.

At the same time, we need to keep saving in a healthy balance in order to avoid hoarding. Believers need to be taught to ask the question, “When is enough, enough?” – and to ask it not just theoretically but practically, putting informed numbers to their saving goals.

The Cautious Debtor

Scripture envisions debt as a consequence of poverty (see, for example, Deuteronomy 15:1-11). In the modern Western world, however, debt often results not from poverty but from materialism and easy availability of credit. While there are some valid reasons and uses for debt, much debt is simply the result of satisfying desires without having saved in advance. And while Scripture does not forbid debt, God warns us consistently of the dangers of debt.

Cautious debtors avoid entering debt, are careful and strategic when incurring debt, and always repay debt. They see debt as potentially dangerous, but not as inherently evil. They understand that all debt is a form of bondage to the lender (Proverbs 22:7) and they realize that debt naturally presumes on the future (James 4:14). When considering taking on a loan, they take these truths into account.

Cautious debtors are patient, content, and intentional. They’re not given to impulse buying (which is the direct cause of so much consumer debt). Their decisions are driven not by culture, marketing, or materialism but rather by a holistic understanding and practice of stewardship.

Cautious debtors are careful and balanced about incurring debt. They make every effort to avoid debt on depreciating assets but consider carefully loans on appreciating items (such as a house). They avoid debt that requires a change in circumstances in order to pay it off (for example, a hoped-for raise or bonus). At the same time, they look for opportunities to leverage debt to create positive results (such as a business or education loan).

Cautious debtors tend to also be wise savers. Because they are patient and content, they’re able to wait to purchase items until they’ve saved for them. And because they place a high value on saving, they’re prepared for circumstances and events that occur. They meet these needs with savings, rather than going into debt.

Equipping Cautious Debtors

Churches need their people to be cautious debtors for several reasons. First, consumer debt fosters envy, greed, and selfishness; these are not the characteristics of a growing disciple of Jesus. Second, debt limits the resources available for generosity. Third, consumer debt is a major trigger of financial hardship, creating bondage and stress for the believer. Believers in this position are rarely able to prioritize growing spiritually and making kingdom impact. Debt becomes an obstacle both to being disciples and making disciples.

Equipping cautious debtors begins with providing a Biblical perspective on money and stewardship. Most consumer debt results from responding to cultural influences rather than to God. Jesus’ warning is a good reminder: “Life does not consist in an abundance of possessions” (Luke 12:15). Similarly, Paul repeatedly warns against materialism and fleshly desires.

As we’ve already seen, Scripture emphasizes the new life of the believer in Christ – both as a reality of salvation (Galatians 2:20) and as an ongoing command (Romans 12:1-2; Colossians 3:1-2). This transformation should bring about, among other changes, a lessening of the pull of the culture and a heightening of focus on treasures in heaven. And this shift in perspective leads believers in turn to become cautious debtors.

Biblical balance in stewardship

Scripture calls believers to a balanced, wise approach to finances that puts God at the center and is characterized by gratitude, contentment, and an understanding of stewardship as opposed to ownership.

While there are examples sprinkled through Scripture of God calling specific individuals to extremes (such as the rich young man in Mark 10), these narratives are not necessarily normative for the church. God called Hosea to marry a prostitute, but He doesn’t call all believers to that!

So God calls us to earn faithfully and diligently, but not to be driven by accumulation of wealth. He calls us to enjoy what he has provided while avoiding selfish materialism. He exhorts us to give systematically, generously, and sometimes sacrificially – but not to be driven by legalism or guilt. He calls us to save wisely while avoiding hoarding. And he urges us to be wise and cautious when incurring debt.

Stewardship Ministry

Discipling our congregations in faithful stewardship requires an intentional focus. As we’ve already seen, many believers have a skewed understanding of financial stewardship (if they’ve thought about it at all). So we know what we need to teach, but how do we teach it?

A stewardship ministry enables a church to engage its congregation in conversation and growth around Biblical financial management. Stewardship ministry can take many different shapes, depending on the size of the church. Some larger churches incorporate an official ministry with a paid staff person leading it; in smaller churches, it’s often led by a staff person with multiple responsibilities or a volunteer.

But however it’s done, the best stewardship ministries – like all discipleship-oriented ministries – rely on the Biblical model of equipping the saints for the work of ministry. In other words, it doesn’t have to fall all on one person! Financial coaches and small group leaders can be an important part of a stewardship ministry.

In many churches, stewardship ministry is closely tied to benevolence. This relationship has some advantages, but may fall short in a couple of areas. First, an approach that sees stewardship only in terms of benevolence may miss out on the discipleship aspect of stewardship. There’s a natural synergy between encouraging generosity in the congregation and providing for needs, but stewardship is much more than benevolence. As we’ve seen, stewardship encompasses all we do with finances for God’s glory. A more holistic approach to stewardship helps the congregation grow in their discipleship in addition to providing for those who need help.

Second, if stewardship is directed only at those in financial trouble, the church may miss the opportunity for kingdom impact from discipling those who are in a better position financially.

Elements of a stewardship ministry

The priorities of a stewardship ministry will be affected by the demographics of the congregation, but here are a few places to consider:

Benevolence. This is the most common starting point and can be addressed in a couple of ways. First, a church can make stewardship training (in the form of a class or an online program or app) a condition of receiving benevolence. This way, the church is helping a person or family not only immediately but also in the longer term, with key Biblical wisdom and practical training to help them get to a place of financial stability and stay there.

Second, a church can train a group of individuals as financial coaches to walk alongside those who are in crisis. Usually, a family or individual in financial crisis took a while to get there, and getting out of trouble is going to take longer than a several-week class. A financial coach can help someone in crisis take what they’ve learned, create a personal plan, and work through implementing the plan. (Note: a financial coach is not an investment advisor! The coach’s job is to help a person move from financial crisis to stability.)

Marriage/pre-marriage. Money is one of the most stress-inducing areas of marriage. A stewardship ministry can help strengthen marriages in the church by enabling couples to get on the same page financially and set Biblical priorities for their resources. What church doesn’t want stronger marriages?!? This is a great opportunity to address a very practical and common stress point in most congregations.

By incorporating stewardship training in a pre-marital counseling program, a church can help couples start off on the right foot. Most couples will come to finances from different family backgrounds and probably have not thought about how they will manage their money as a couple. Indeed, most don’t have a framework for even having that conversation. A stewardship training ministry can help couples discover their financial position and work through priorities and a plan.

Youth ministry/Parenting. Most parents don’t feel qualified to teach their kids about finances. Perhaps they’ve made mistakes in the past (and maybe they’re still living with the consequences). Or maybe they feel that the way they’ve handled finances won’t resonate with their children. Whatever the cause, many parents need help raising their children to be faithful stewards – just like they need help in other areas of discipling their kids.

A stewardship ministry can help train parents in their own stewardship and can equip them with age-appropriate ways to train their children.

Singles/Men’s/Women’s ministry. In most congregations, a significant number of people are “struggling in silence” with finances, and they don’t know where to turn to for help (or even that help might be available). Ministries like Adults, Singles, Men’s, or Women’s ministries can help disciple believers with stewardship training. This training may uncover a need for coaching for some; for others, it may result in a shift in priorities that frees up resources for the kingdom.

Small Groups ministry. Life-change happens in small groups. Many churches recognize that and place a high priority on small group ministry. A stewardship training program designed for small groups can not only disciple individuals in stewardship but also provide encouragement and support through the small group structure. Inter-generational groups and groups comprised of people in different financial situations are particularly helpful, as members can help others overcome problems that they have dealt with.

Keys to effective Stewardship ministry

Whether your church is large or small, you can have an effective stewardship ministry. Here are a few keys to starting and maintaining a stewardship ministry that makes a difference in your congregation.

- Make it front and center. In any church, what gets said from the front carries weight. Jesus didn’t shy away from the topic, and neither should we. Messages on stewardship and announcements about stewardship training help the congregation understand the importance of this key area.

- Make it about discipleship. Stewardship is more than giving and it’s more than getting out of debt. Money is a chief rival god, and managing it well brings honor to God and growth in following him. Treat stewardship holistically and anchor your teaching in Scripture, and the congregation will see it as a key area of spiritual growth and discipleship.

- Make it for everyone. Because stewardship is a key area of discipleship, it’s important for the whole congregation. Not just those in debt. Not just those who fund the church’s operations. Jesus interacted with people from across the financial spectrum, and the crux of his message was, “Where your treasure is, there your heart will be also.” Regardless of the size of our treasure, we all want our hearts to be focused on heaven.