Contents

- The Cautious Debtor

- Characteristics of a Cautious Debtor

- Practices of a Cautious Debtor

- The Dangers of Debt

- Spiritual Dangers of Debt

- Economic Dangers of Debt

- Is Some Debt OK?

- Two Guidelines

- Types of Debt

- Managing Debt Wisely

We live in a culture where debt is pervasive. College students and recent graduates are in debt. Families are in debt. State governments are in debt. Our federal government is over $30 trillion in debt, with no plan to repay it.

The easy availability of credit, combined with an increasingly materialistic culture, leads to a couple of key myths about debt:

- Debt is expected and unavoidable.

- As long as we’re keeping up with the minimum payments, we’re OK.

On the other side, some church teaching has condemned debt as sinful and to be avoided at all costs.

As is usually the case, the truth lies somewhere in the middle. In this article, we’ll look at the Bible’s teaching about debt, evaluate whether some debt is OK, and outline principles for managing debt wisely.

Debt in the Bible

The assumptions regarding debt in Biblical times differ from today’s assumptions. Originally, debt was assumed to be the result of poverty – not something that someone would willingly enter into. Debt wasn’t portrayed as sinful; instead, it was an unfortunate (and sometimes inevitable) consequence of destitution. The fact that there would be those in Israel who lived in poverty was a foregone conclusion (Deuteronomy 15:11).

As a result, God provided multiple ways for those who were indebted to regain their financial footing. This enabled families to escape generational poverty.

- Every seven years, the Israelites were to cancel any debts owed to them by their fellow Israelites (Deuteronomy 15:1-11)

- Every 50 years, the Israelites were to celebrate the year of Jubilee, when those who had sold lands (usually due to poverty) could reclaim those lands and those who had sold themselves as servants regained their freedom (Leviticus 25).

Debt Today

Today, the context of debt is much different. While there are still those who incur debt as a result of poverty, government programs forestall this necessity in most cases. Instead, most debt today is voluntary and is the result of decisions we make.

A culture of prosperity, materialism, and impatience – combined with the easy availability of credit – leads us to purchase things we don’t have the money for, so we incur debt by using credit cards. Marketers take advantage of this tendency (and even create some of it) by fostering a sense of discontentment with what we have, how we look, or how we live. The cultural norm of entitlement (“You deserve a break today”) leads us to believe that we deserve better, so we buy it – whether or not we have the money.

And purchasing has never been easier. “One-click” shopping puts debt merely a click or tap away on shopping websites. Payment apps, recurring subscriptions that require no intervention (remember how you used to have to do something to renew a magazine?), online transfers – we have more ways to spend money now than we have money to spend! And so the debt piles up.

Additionally, we take on debt to accomplish key goals that are nearly impossible otherwise, such as a college education or owning a home. We commonly take on debt to purchase large items such as cars or appliances.

Since the vast majority of debt today is voluntary, we have an opportunity to control it by exercising caution and wisdom.

The Cautious Debtor

The Cautious Debtor is one who avoids inefficient debt, is careful and strategic when incurring debt, and always repays debt.

Those who are cautious with debt exhibit several Biblical characteristics and practice a couple of key strategies.

Characteristics of a Cautious Debtor

Cautious Debtors don’t necessarily fear debt and they don’t treat it as something to be avoided at all costs. But they manage debt wisely so that it doesn’t control their lives. They resist temptation that leads to debt and plan expenditures wisely. Their relationships to debt stem from several Biblical character qualities.

But the fruit of the Spirit is love, joy, peace, forbearance, kindness, goodness, faithfulness, 23 gentleness and self-control.

Galatians 5:22-23

Make every effort to add to your faith goodness; and to goodness, knowledge; 6 and to knowledge, self-control; and to self-control, perseverance; and to perseverance, godliness; 7 and to godliness, mutual affection; and to mutual affection, love.

2 Peter 1:5-7

Faith

Cautious Debtors believe in God’s provision. So they’re not prone to run ahead of that provision and incur debt trying to provide for themselves. They trust that not only will God provide, but also God is providing – that is, that what they have is all they need based on God’s provision. This faith leads to a couple of other key characteristics: gratitude and contentment (see Philippians 4).

Peace

Peace can take many forms and can be about many things, but a common element is always lack of anxiety. When it comes to debt and spending, peace about our circumstances can prevent us from trying to “keep up” with a culture that lives in desperate pursuit of material possessions. Paul links together God’s peace with an attitude of grateful prayer (Philippians 4:6-7). God promises peace as we trust in him:

You will keep in perfect peace

those whose minds are steadfast,

because they trust in you.

Isaiah 26:3

Self-Control

Self-control gives us the discipline to say “no” to instant gratification. It enables us to stay within our Spending Plan, keeping us from impulse buys that lead to credit card debt. Self-control doesn’t come naturally; it’s a fruit of the Spirit working in our lives. At the same time, it’s something we’re called to exercise.

Perseverance

Where self-control protects us in the moment from impulsive spending, perseverance does the same thing over the long run. Perseverance enables us to save up for our purchases, rather than going into debt to make a purchase quickly.

Practices of a Cautious Debtor

These characteristics enable the Cautious Debtor to faithfully adhere to three key practices: avoiding inefficient debt, strategically incurring debt, and committing to repaying debt.

Avoiding Inefficient Debt

In today’s economy, there is such a thing as efficient debt – that is, debt that can be leveraged for positive purposes with minimal financial disadvantage. We’ll talk more about that later. Inefficient debt – that is, debt that’s incurred on things that depreciate or on experiences – is the kind of debt that gets us in the most trouble with credit cards. Cautious debtors avoid this kind of debt.

Incurring Debt Strategically

The Cautious Debtor understands the difference between efficient and/or necessary debt and the inefficient debt we just talked about. When incurring debt, cautious debtors make sure that they’re doing it for strategic reasons rather than impulsive responses. And they take care that the amount of debt they undertake makes sense for the financial leverage it might provide (more on this later).

Repaying Debt

While the Bible doesn’t forbid debt or call it sin, Scripture definitively requires that the borrower repay debt:

The wicked borrow and do not repay

Psalms 37:21

As a result, cautious debtors do whatever it takes to repay debt – always. Recognizing debt as an obligation, they eschew easy ways out like bankruptcy or student loan forgiveness. They’ve given their word, and as image-bearers of a promise-keeping God, they’re bound to keep that word.

The Dangers of Debt

It’s tempting to treat debt just like any other bill – after all, we make monthly payments on it just like we do for our utilities, car insurance, or other bills. But debt isn’t like other bills in a couple of significant ways.

The rich rule over the poor,

Proverbs 22:7

and the borrower is slave to the lender.

Debt enslaves us. Paul tells us that Jesus set us free in order for us to enjoy freedom (Galatians 5:1). He says this in the context of warning the Galatians against being enslaved to the law; but the principle applies also to debt. As we’ve seen, debt must be repaid – so when we have debt, we’re not free to give, save, or spend as we might like. We’re obligated to repay.

Remember what we said earlier about debt in ancient Israel? It often resulted in literal slavery or servitude. We don’t typically experience such a visible impact from debt today, but the concept remains. The borrower is still slave to the lender.

The obligation to repay debt also takes away our freedom in another way. With other bills, if we find we can’t afford them, we can often make adjustments – we can cut cable, reduce some utility usage, cancel subscriptions, etc. These expenses are current expenses, so we have power to alter them.

But debt represents a past expense, and we can’t change the past. It doesn’t matter whether or not we can afford the payments – we’ve obligated ourselves to make them anyway. This can lead to a spiraling situation in which financial freedom eludes us.

Spiritual Dangers of Debt

Let no debt remain outstanding, except the continuing debt to love one another.

Romans 13:8

Besides the above general dangers, there are specific spiritual and economic dangers related to debt. Spiritually, debt presumes on and encumbers the future. It denies God the opportunity to provide for us or to teach us through denial, and it fosters envy and greed.

Presuming on the Future

All debt carries one basic assumption – that we’re going to pay it back. No honest person takes on debt without planning to repay it; and no lender loans out money thinking they won’t get it back. But all of this makes certain assumptions about the future – assumptions that jobs will continue, that other critical expenses won’t arise, etc. James warns us against presuming on the future (James 4:13-15). Such presumption is boastful in the sense that we’re assuming we control events that we really don’t control.

Encumbering the Future

On a related note, debt also encumbers the future, and this can have major spiritual implications. Many a college student, zealous for God’s glory among the nations, has found that school debt stands in the way of going to the mission field. Many believers, convicted by the Holy Spirit of the priority of giving, find themselves constrained by past decisions that led to significant credit card debt.

Debt limits our opportunities to serve God and can hinder our spiritual growth. Perhaps this is why Paul advised against allowing debt to remain outstanding. The writer to the Hebrews puts it this way:

Let us throw off everything that hinders and the sin that so easily entangles. And let us run with perseverance the race marked out for us.

Hebrews 12:1

While debt itself is not sin, it can represent one of the biggest hindrances to running the race that God has marked out for us.

Denying God Opportunity

God has promised to take care of us when we seek his kingdom first, meeting our needs (Matthew 6:25-33; Luke 12:22-31). Often, times of need provide the greatest opportunity for God to work in our lives. Think of the miracles in Scripture where God showed his power by working in times of need! Here are just a few:

- God provided miraculously for a widow in Zarephath whose flour was about to run out, as she took care of Elijah (1 Kings 17); this miracle was so distinct that Jesus even called it out (Luke 4:26)!

- Similarly, God provided for a widow whose husband had been one of the prophets, protecting her from having to sell her sons into slavery (2 Kings 4:1-7).

- Jesus twice fed crowds of thousands with minimal loaves and fish that he multiplied (Matthew 14, 15).

When Jesus challenged the disciples to feed the crowd, they responded with incredulity – not only did they not have that much food, there was no way they could have gotten it. Picture Peter, James, and John running to the local Costco with their platinum card and filling cart after cart of food, trying to meet the incredible need with money they didn’t have! A major miracle would never have happened. And yet, that’s how we often respond to our own needs. Rather than trusting God to do what we can’t, we charge ahead and charge our purchases.

In addition to miraculously providing for us, sometimes God wants us to teach us through need. Recall Paul’s thorn in the flesh (2 Corinthians 12:8-10). Paul earnestly pled with God to remove it, but instead God used it to teach him an important lesson.

God often brings his people to a point of need in order to glorify himself through miraculous provision or through maturity of his followers. Around the world, Christians in desperate situations often see God come through in unanticipated ways. In the West, we don’t see that as often – most likely because we run ahead of God to meet our own needs with debt.

Fostering Envy and Greed

“Watch out! Be on your guard against all kinds of greed; life does not consist in an abundance of possessions.”

Luke 12:15

In addition to presuming on the future and denying God opportunity to provide for us and to teach us, debt tends to foster envy and greed. Jesus warned us that our lives don’t consist in the abundance of our possessions. Today, the availability of credit allows us to have what we want, when we want it. This makes us easy pray for marketers, who are constantly finding new ways to entice us to spend money we don’t have on things we don’t need. (Have you ever noticed in commercials that all men who use a certain razor are in their prime, with impressive physiques and perfect hair?)

Not only does debt foster envy and greed, but it also short-circuits gratitude. When we save up over time for something we really want, we purchase it with a grateful heart and enjoy it more fully. When we put the same purchase on a credit card, without investing the time and energy to save, not only do we appreciate the item less, but our joy is impacted by the additional debt load we now have to worry about.

Economic Dangers of Debt

In addition to the spiritual dangers of debt, there are several economic dangers. These revolve primarily around compound interest working against the debtor, and the impact on margin in the Spending Plan.

The Downside of Compound Interest

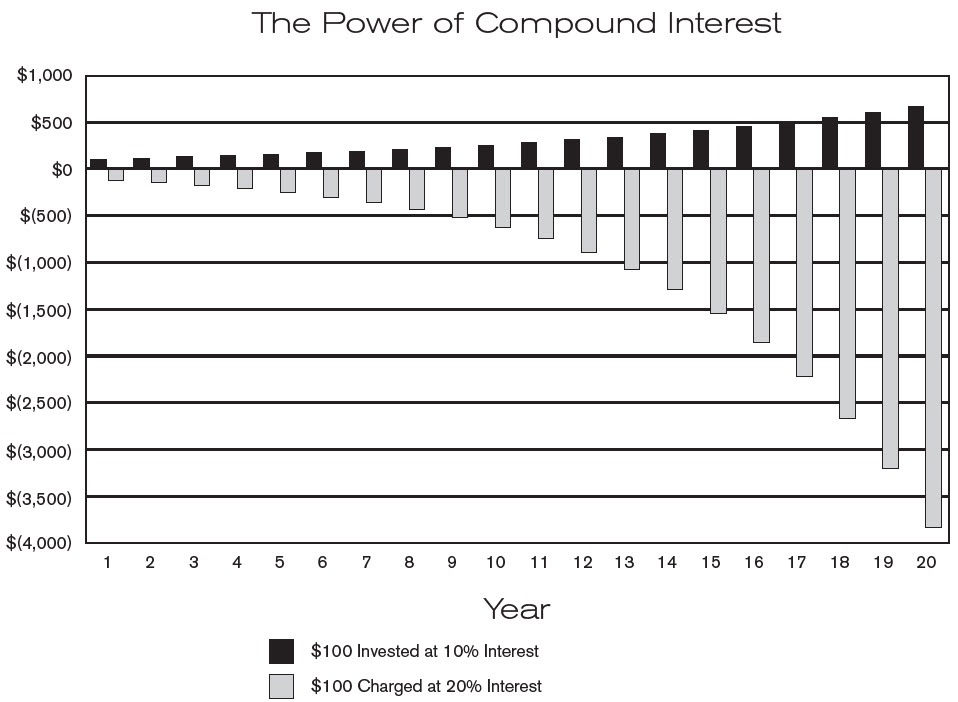

Compound interest means basically, “interest on interest”. And while compound interest works in favor of the saver, it works against the debtor.

The below chart shows the relative financial positions after 20 years of two people. The first person invested $100 at the beginning of the 20 years at 10% interest and did not touch the account after that. The second person borrowed $100 at the beginning of the 20 years at 20% interest and made no payments. (And yes, unfortunately, the interest rates paid by debtors typically far exceed the interest rates paid to savers!) Over the course of 20 years, note the difference in both direction and amounts:

After 20 years, with nothing but interest working, the saver has around $700 to show for his $100 investment. But the debtor who borrowed just $100 now owes nearly $4000!

This is a simplified way of showing the impact of compound interest. In a real-life scenario, of course, the debtor would actually be making payments, not just letting the debt sit there. But compound interest still works against the debtor even while repaying debt.

Look at a recent credit card statement and compare the interest charge for the month to the minimum payment. If your account is like most, the majority of the minimum payment is paying interest, not reducing the balance of the card. It’s like trying to walk up a downward escalator.

Zero-interest debt

Even in scenarios that don’t involve interest, debt still carries an economic danger. Most “zero-interest” purchases come with a catch – a credit card that must be paid off in a relatively short period of time. If not paid off in that time, interest is charged retroactively to the date of purchase. Many a customer has had a very unpleasant surprise at the end of the grace period when they weren’t able to pay off the entire balance. Credit card companies count on this – this is why they make these offers.

When considering any consumer debt, we should ask a couple of key questions:

- Is there an alternative to the debt? (For example, can I use a laundromat while saving up to replace my washer?)

- If I haven’t been able to save up for the purchase yet, what is going to change to enable me to make the payments?

Reduction of Margin

Similar to the way that debt encumbers the future, it also encumbers the present in the form of reduction of margin in our spending plans. Money that could be going to giving, saving, or other spending opportunities is instead devoted to repaying debt.

Over time, inflation tends to increase our need for money in areas like groceries and clothes. But when significant debt is present, it becomes much more difficult to find the extra money to meet the increased needs in these areas. As a result, debt makes us more vulnerable to all kinds of occurrences, from swings in the economy to unforeseen personal needs.

Is Some Debt OK?

We’ve said earlier that debt is not inherently sinful. In fact, there are occasions in today’s economy and culture where debt actually can bring some benefits. The dangers listed above still apply and should be taken into account; however, there are some occasions where the benefits of carefully considered debt may outweigh the dangers. Remember, part of the definition of the Cautious Debtor is one who is careful and strategic when incurring debt.

Two guidelines

While situations vary, two key guidelines can help in determining whether a given debt decision makes sense:

- Is it being incurred on something that increases in value (eg, a house)?

- Can it be repaid under today’s circumstances?

Debt incurred on depreciating assets, such as cars and appliances, is by nature inefficient. There could be cases where such debt is a necessity (for example, if public transportation isn’t available, a car may be a necessity in order to get to a job). But there’s always a danger – if at some point the payments cannot be made, it may not be possible to sell the asset purchased to pay off the balance, because the asset is decreasing in value. Contrast this with a house, which typically (though not always) increases in value over time.

One key question to ask is whether debt can be repaid if nothing else changes. Taking on a debt that requires a raise in order to pay it off increases the economic danger of the debt (not to mention presuming even further on the future). One exception to this guideline is education debt (we’ll talk more about this shortly).

Types of Debt

There are many ways to characterize debt to help guide decisions. Generally, debt falls into one of two categories: efficient debt, and inefficient debt. This doesn’t always equate to “good” debt and “bad” debt; it’s possible for an efficient debt to be unwise and for an inefficient debt to be necessary.

Efficient Debt

Efficient debt generally meets the two guidelines above and further is being leveraged for a positive purpose. Examples include:

- Housing: Most of us will pay for housing in the form of rent or of a mortgage. While a mortgage is not always a better idea than rent, there are often advantages to leveraging debt this way. Additionally, mortgages tend to have the lowest interest rates of any kind of debt.

- Education: College education most often leads to some debt. College debt is dangerous in that it depends on hoped-for circumstances to be repaid; we assume that we’ll be able to get a job that pays enough to allow us to repay the loan and make a living. But this is the kind of debt that’s being leveraged for a positive purpose – to increase our earning capacity.

- Business: Starting a business often requires debt in order to make the initial capital investment. But businesses not only provide income, they also have other benefits to society, such as providing a service or employing others.

Inefficient Debt

Inefficient debt is, well, everything that doesn’t meet the above characteristics. It’s usually incurred on something that depreciates in value. All consumer debt (credit cards, etc.) is inefficient by nature. Some of that debt may be necessary, such as a medical emergency or a need for transportation. But this is the type of debt that should be avoided as much as possible.

Managing Debt Wisely

As we’ve seen, Scripture does not forbid debt. But debt carries multiple dangers, both spiritual dangers and economic dangers. One key question to ask when considering debt is, “Can I repay this debt without being enslaved by it?”

Scripture requires that debt be repaid (Psalm 37:21). So when taking on debt, we need to be as sure as possible that we can repay it. Obviously, this requires a certain amount of presuming on the future, so we need to make these decisions wisely and prayerfully.

Besides being able to repay debt, we also need to be sure that the debt doesn’t dominate our lives. We’ve seen that the borrower is slave to the lender (Proverbs 22:7). This means that the borrower has another master besides God – and we’re called to serve God alone. Debt can become so burdensome that we’re not free to serve God as he calls us to. Again, this doesn’t mean that all debt is wrong – but rather that we shouldn’t take it lightly.

Make a Plan

It’s impossible to manage debt wisely without a Spending Plan. This should be obvious – without a spending plan, we don’t really know how much we can afford in terms of payments. And without a spending plan, we don’t have the tools we need in order to evaluate the impact of a debt decision on our other financial priorities.

Having a working current Spending Plan is the first step. The second step is updating that plan with the proposed debt payments. What adjustments will be required in other spending areas in order to support the debt payments? Here are a couple of thoughts to consider:

- If the payments will negatively impact giving, then the spiritual danger may outweigh any benefit to be gained.

- If the payments will negatively impact saving, then the economic danger may outweigh the benefit.

- If the payments can be made by adjusting spending areas other than giving and saving, consider the impact of those adjustments on other lifestyle areas. Is the debt worth the cost of reducing spending in other areas?

Create a Buffer

Remember how we said that the Cautious Debtor avoids debt? One of the keys to successfully avoid debt is to have sufficient savings to cover unexpected events.

A medical emergency occurs. One person incurs a $3,000 debt to cover their part of a hospital bill; another simply pays that bill out of what they’ve saved in their Health Savings Account.

An appliance breaks down. One person puts $1,500 on a credit card to replace it; another buys it with replacement savings already set aside.

A surprise car repair comes up. One person charges $1,000 on a credit card to get the repair made; another pays for it out of Emergency Savings.

As it turns out, cautious debtors are also wise savers. They understand that needs will arise and they build into their spending plans sufficient saving to prepare them for those surprises. Check out our article, Biblical Wisdom on Saving, for more details.

Think it Through

We’ve seen that some debt can be considered efficient debt due to the purposes for which it’s being leveraged – housing or education, for example. However, that doesn’t make these types of debts necessarily wise. And just because a debt is necessary (to buy a car, for example), that doesn’t mean that a specific debt decision is a good one.

Debt is not a binary decision – it’s not a “yes” or “no”. A key aspect of all voluntary debt decisions is how much debt is wise to take on. So, for example, it’s probably not a wise decision to buy a brand new $30,000 car on credit in order to get back and forth to work. A better decision would be to take on less debt and purchase a good used car, saving up for the next car when this one is paid off.

Similarly, committing to $40,000/year to attend a prestigious out-of-state university in hopes of getting a $40,000/year job probably creates more financial pressure than needed. A better decision might be to attend a community college for the first two years and then go to an in-state school; or possibly to consider a trade school or other avenue.

The same is true with a mortgage. The fact that a mortgage can be “efficient debt” doesn’t mean that a specific mortgage is a good idea. Everyone involved in a real estate transaction is financially motivated to maximize the price of the transaction (except, of course, the buyer). Many home buyers have found themselves “house poor” after getting a loan at the maximum amount they could get approved for. Other home buyers have been surprised at the hidden costs of upkeep and improvements – owning a house is financially much more complex than renting.

Cautious debtors are careful and strategic when entering debt. They weigh the pros and cons of any debt decision. They consider alternatives and look to maximize their cost/benefit ratio.

Don’t Kick the Can

One key danger of debt is the temptation to “kick the can down the road” with a debt consolidation loan or balance transfers to a lower-interest credit card (typically the lower interest doesn’t stay that way!). There are several dangers with this:

- This type of activity always has a negative impact on the borrower’s credit score. This can have multiple financial effects.

- These types of transactions don’t address the problem that caused the debt in the first place. If the problem is overspending (which is the cause of most debt), then transferring debt to a new vehicle doesn’t solve that problem; in fact, it creates another one.

- Balance transfers and debt consolidation loans increase the total credit limit available (unless you close out the credit cards you’re transferring from). This increases the danger of going further into debt if the overspending problem is not addressed.

Pray!

If any of you lacks wisdom, you should ask God, who gives generously to all without finding fault, and it will be given to you.

James 1:5

Prayer is not usually our first instinct when it comes to making financial decisions, but it should be. And decisions involving debt need more prayer than many, due to the spiritual and economic dangers involved.

When we pray over decisions like taking on debt, our posture should be one of asking God questions and seeking his guidance, not of giving him the answers and asking him to bless what we’ve already decided. Prayer that assumes the answer runs into the danger of being wrongly motivated.

You do not have because you do not ask God. 3 When you ask, you do not receive, because you ask with wrong motives, that you may spend what you get on your pleasures.

James 4:2-3

Here are a few suggestions for approaching these decisions before God:

- Thank God for what he has already provided in your financial situation.

- Lay out the need before God. Ask for his provision to meet the need.

- Ask God to show you his priorities. Start at a high level (not, “which house should I buy?” but “How can I live so that you are honored in my finances?”)

- Ask God to show you what you need to know in order to make a good decision (he sees the future; we don’t!).

- Pray over specific decisions (Is this the right path? Is there a different path I should be pursuing?).

Taking on debt entails significant dangers, both spiritual and economic. Still, efficient debt can be leveraged for positive, even God-honoring purposes. In light of this, cautious debtors take these decisions seriously and take them to God.