Paying Down Debt

One of the many myths regarding the use of credit cards is that, as long as we’re making the minimum monthly payments, we’re OK. But even assuming that we incurred no new debt on a credit card, making the minimum payments will maximize the amount of time it takes to get us out of debt.

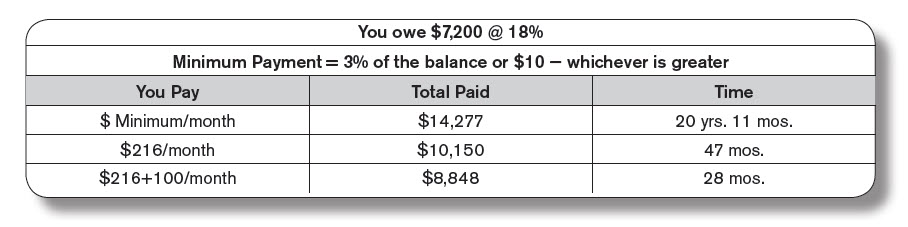

Consider the below example, in which a debtor owes $7,200 on a credit card charging 18% interest, with a current minimum payment of $216:

In the first line above, the debtor repays the credit card making minimum payments each month, without incurring any new debt on the card. Note that the minimum payments decrease as the balance decreases, so the actual amount being paid each month gets smaller and smaller. This is why it takes so long to pay off a credit card with just minimum payments. And note that the total amount paid is nearly twice the principal.

In the second line, the debtor keeps the credit card payments consistent at $216 per month, the minimum payment of the current month. If there is room in the budget for that payment this month, then there should be room every month for that payment. Note the dramatic difference in repayment time – down from almost 21 years to just under 4! In addition to that, the total amount paid decreases by over $4000.